As the manufacturing sector settles into 2026, the convergence of AI-driven automation, shifting trade policies, and evolving workforce expectations is redefining operational competitiveness. Success in this complex landscape will depend on a strategic balance between technological innovation and human-centric workforce agility to ensure long-term stability and growth. We’ll break down how AI and automation are reshaping production and decision-making, where trade policy and tariffs are influencing sourcing and cost structures, and how workforce expectations are shifting toward flexibility, purpose, and upskilling.

Trend #1: AI Can Accelerate Hiring. But It Can’t Replace Workforce Strategy.

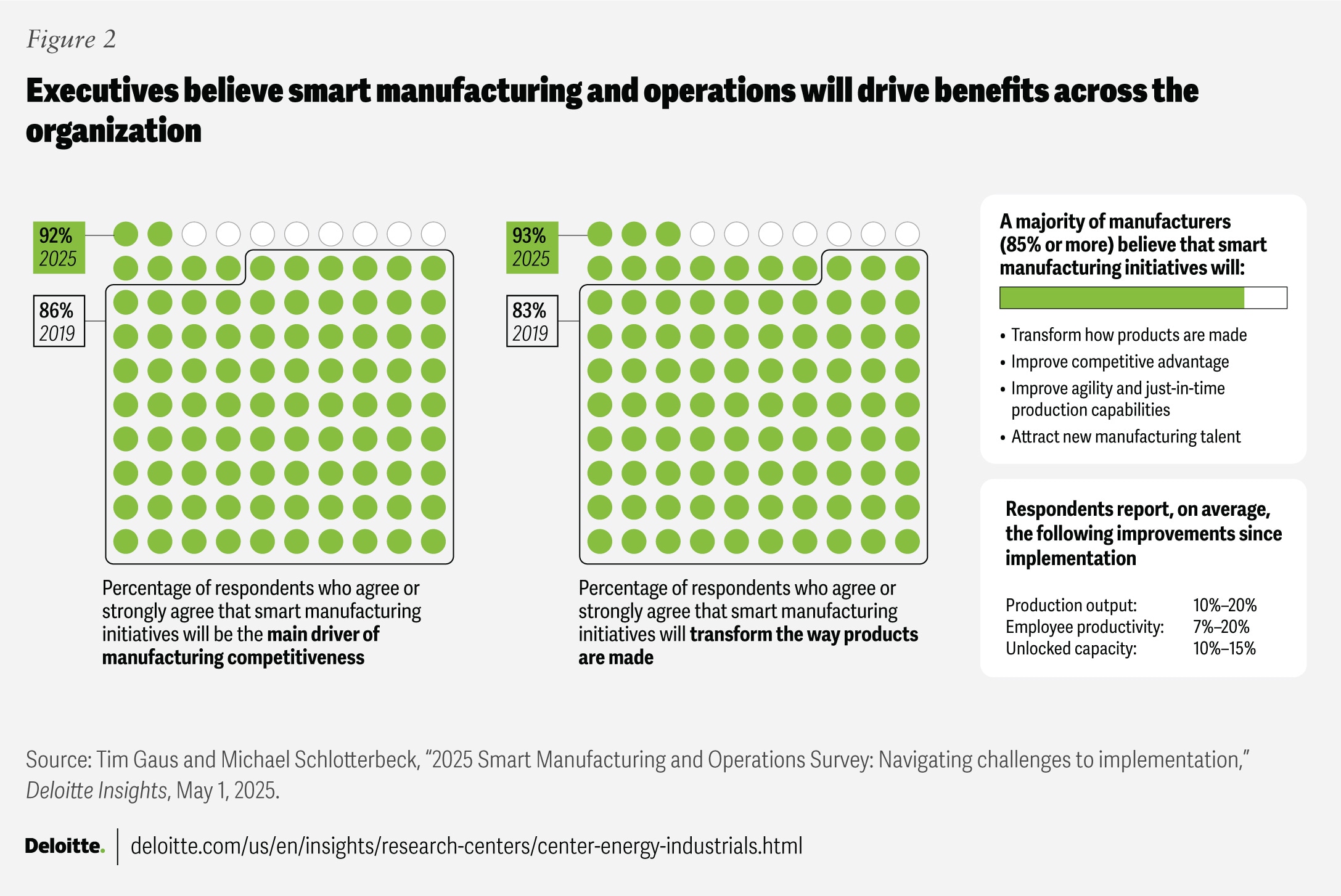

AI and automation are no longer “future concepts” in workforce staffing, accelerating hiring, and improving predictability by handling high-volume tasks like sourcing and scheduling. In manufacturing, AI is increasingly used for predictive maintenance, quality assurance, and intelligent scheduling, making production floors smarter and equipment self-monitoring. This evolution is transforming traditional operator roles into tech-enabled positions requiring both hands-on skill and technical literacy. Reflecting this trend, Deloitte’s outlook shows that 80% of manufacturing executives plan to invest 20% or more of their improvement budgets in smart manufacturing initiatives in 2026. By 2026, IDC finds that over 40% of manufacturers with production scheduling systems will upgrade to AI-driven autonomous scheduling. However, technology alone cannot solve workforce instability. While AI can fill roles faster, human factors such as trust, engagement, and stability remain crucial for retention and production continuity. The optimal approach is augmentation, where AI removes friction, allowing humans to focus on critical tasks.

There are risks, of course. Poor data leads to poor decisions. Over-automation erodes trust. Bias, compliance, and transparency must be managed. Technology doesn’t fix broken processes; it scales them. The organizations that will win are not those who automate everything, nor those who resist change, but those who strike the right balance. The winning strategy involves striking a balance between automation and human involvement, focusing on integrating solutions for hybrid technical roles, investing in upskilling, and leveraging contingent workforces to pilot AI-driven environments.

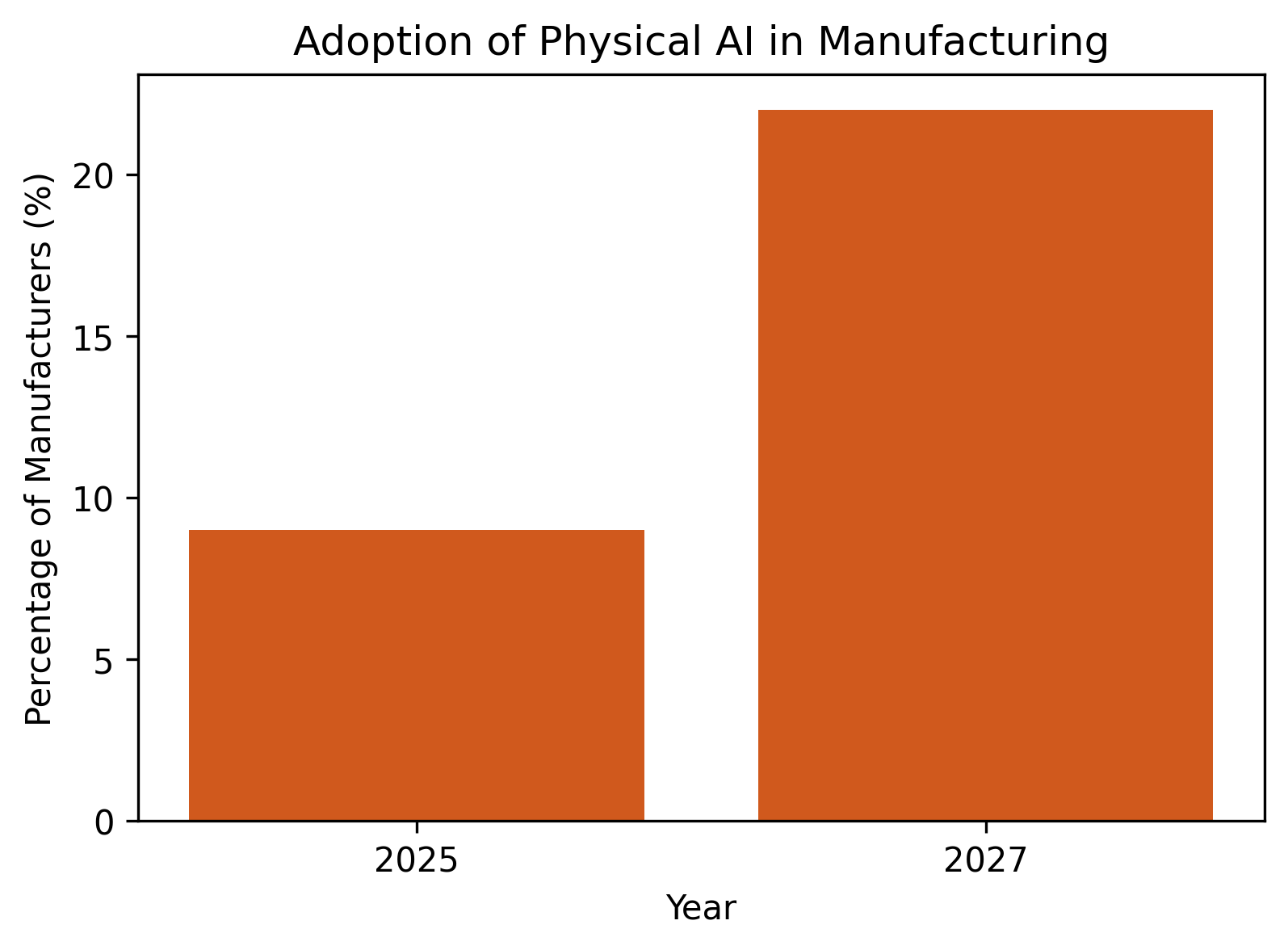

The fundamental idea is clear: AI excels at speed, scale, and generating insights, while people provide judgment, reliability, and trust. According to Gartner, global spending on AI is expected to hit $2.52 trillion in 2026, a 44% rise compared to the previous year. Additionally, Deloitte reports that 22% of manufacturers plan to adopt physical AI, such as more autonomous robotics by 2027, doubling from 9% in 2025.

Trend #2: How Manufacturers Are Adapting to Tariffs Without Slowing Down

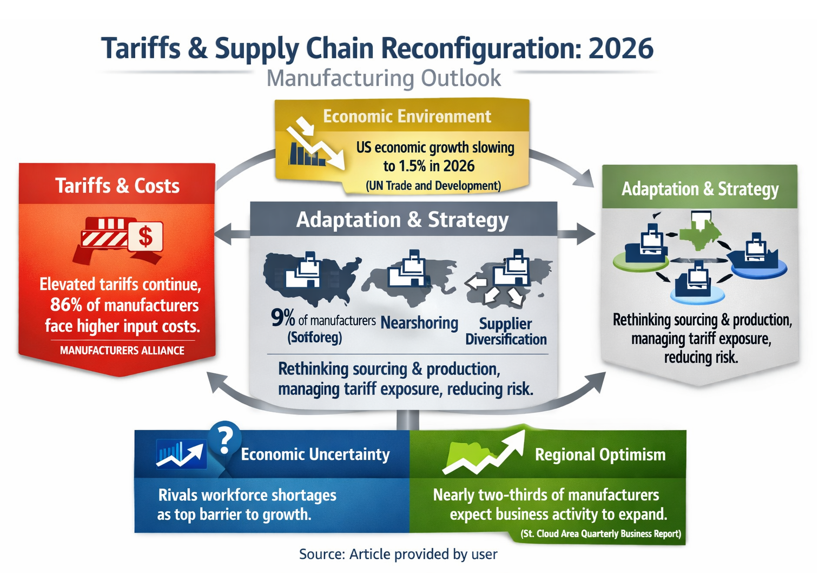

Despite pressures from elevated tariffs continuing from last year, manufacturers have adapted rather than pulled back. The Manufacturers Alliance reports that 86% of manufacturers are facing higher input costs, yet many continue to operate by rethinking sourcing and production strategies.

Reshoring has gained momentum, with FORBES reporting that 9% of manufacturers are already bringing production back to the U.S., more than double the level seen just a few years ago. Others are turning to nearshoring, bringing production closer to home, and supplier diversification to manage tariff exposure and reduce risk.

At the same time, the broader economic environment is cooling. According to UN Trade and Development, the U.S. economic growth is projected to slow to 1.5% in 2026, down from 1.8% in 2025, adding another layer of uncertainty. Recent manufacturing surveys indicate that economic uncertainty now rivals workforce shortages as the top barrier to growth, highlighting how interconnected cost pressure and labor challenges have become.

Still, optimism persists at the local level. One example of this is the St. Cloud Area Quarterly Business Report, showing that nearly two-thirds of manufacturers expect business activity to expand, with some anticipating payroll growth, even as hiring qualified workers and retaining talent remain ongoing challenges. This trend isn’t isolated – similar optimism is emerging across regional markets throughout the U.S., reinforcing a broader pattern of cautious but steady growth.

As supply chains reconfigure and production footprints shift, labor needs are becoming more regional and less predictable. Job opening data, from the Bureau of Labor Statistics, show significant variation by state, reinforcing that labor shortages are uneven and often tied to where reshoring and nearshoring are occurring. According to Deloitte, manufacturers are increasingly relying on flexible workforce models, for example, blending full-time and contingent labor to maintain production during demand swings and material volatility.

Trend #3: Workforce Demographics and Expectations

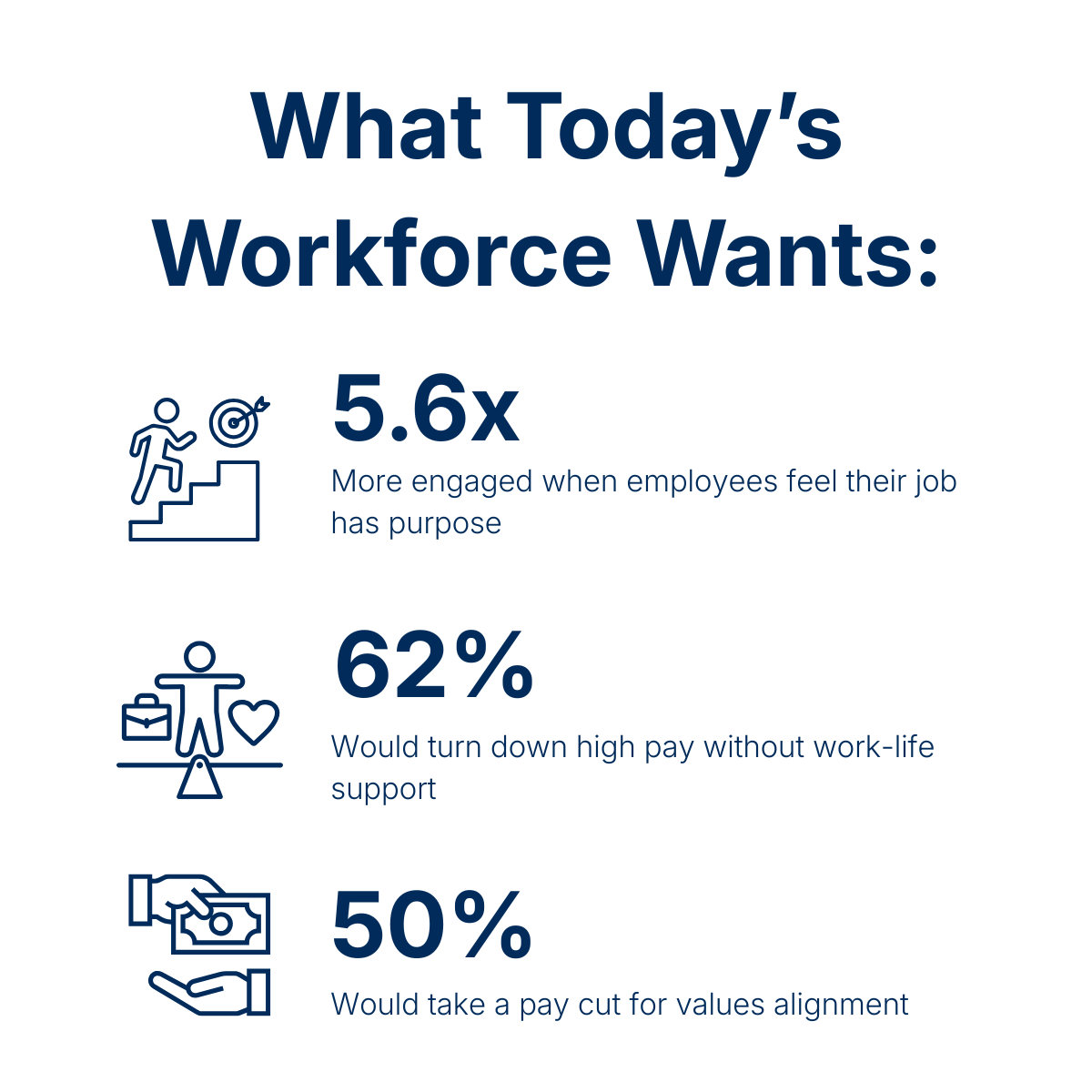

Today’s workers aren’t just chasing higher wages; they’re chasing work that fits into their lives and supports their long‑term well‑being. Gallup reports that only about 18% of employees say their job has a purpose they personally believe in, and just 12% feel their work supports broader life meaning. Those who find purpose are far more engaged – 5.6 times more likely, in fact. Meanwhile, Checkr survey finds that 62% of workers say they would turn down a high‑paying job if the benefits didn’t support their life outside of work, and nearly half would take a pay cut to work at a company aligned with their values and growth.

These trends make clear that modern employees expect employers to help remove barriers to a fulfilling life, not just offer a paycheck. When it comes to manufacturing workers, the pressure of finding sustainable housing and transportation can be a significant barrier to success. Eliminating these stressors can clear up a significant amount of free time and allow them to focus on other aspects of their life.

Why Regulatory Pressure Is Forcing a Rethink of Workforce Strategy

Despite growing volatility in labor demand and intensifying regulatory pressure nationwide, manufacturers now face both risk and opportunity. Recent reporting from Mosey shows that 33% of multistate employers incurred compliance penalties in the past year, underscoring how costly misalignment has become.

While the expanding scope of labor enforcement presents challenges, it is also pushing organizations to modernize outdated workforce processes. Many manufacturers are tightening pay and contract accuracy, improving transparency, and adopting more efficient workforce models designed to reduce long‑term risk.

As regulations evolve across worker classification, immigration, and AI‑supported hiring, forward‑looking employers are using these shifts to their advantage. Rather than reacting to compliance issues after they occur, they are implementing smarter systems that anticipate workforce needs and regulatory requirements in advance.

The cost of inaction is significant. According to the Metal Service Center Institute, federal regulations now cost small manufacturers an average of $50,100 per employee annually. In response, many organizations are streamlining multistate reporting and improving audit readiness to unlock productivity and redirect resources toward growth.

Taken together, these pressures are not slowing progress; they are accelerating it. Manufacturers are increasingly turning to agile, mobile staffing solutions that provide greater flexibility, operational continuity, and the workforce’s adaptability required to compete in a rapidly changing environment.

Strategic Implications for Manufacturers

Manufacturers today are operating in an environment where technological advancements, global economic pressures, and workforce dynamics are no longer separate challenges; they are factors shaping competitiveness. The rise of AI is changing how work is performed, but it does not eliminate the need for labor.

At the same time, tariffs and shifting trade policies continue to impact material costs and supply chain decisions, putting pressure on margins and increasing the need for operational flexibility. These forces converge most directly in the workforce, where labor shortages, rising expectations, and compliance complexity can either limit growth or become a strategic advantage.

In this environment, workforce agility has become a critical form of competitive differentiation. Manufacturers that can scale labor up or down quickly are better positioned to respond to fluctuating demand, unexpected disruptions, or new production opportunities. Rather than reacting to labor shortages or market shifts, agile manufacturers proactively design workforce strategies that support production goals and protect profitability. Organizations with agile labor strategies can maintain momentum during growth periods while avoiding the operational strain that comes with being understaffed or overextended.

Sources

Deloitte Insights. 2025 Smart Manufacturing and Operations Survey: Navigating Challenges to Implementation.

Deloitte Insights. Manufacturing Industry Outlook 2026.

IDC. Worldwide Manufacturing Insights: AI-Driven Production Scheduling Forecasts.

Gartner. Forecast Analysis: Artificial Intelligence Global Spending, 2026.

Manufacturers Alliance. Manufacturing Cost and Tariff Impact Report.

Forbes. Reshoring Trends in U.S. Manufacturing.

United Nations Conference on Trade and Development (UNCTAD). Global Economic Outlook 2026.

U.S. Bureau of Labor Statistics (BLS). Job Openings and Labor Turnover Data (JOLTS).

St. Cloud Area Chamber of Commerce. Quarterly Business Report.

Gallup. State of the Global Workplace Report.

Checkr. Workforce Trends and Employee Expectations Survey.

Mosey. Multistate Employer Compliance Report.

Metal Service Center Institute. Regulatory Cost Burden for U.S. Manufacturers.